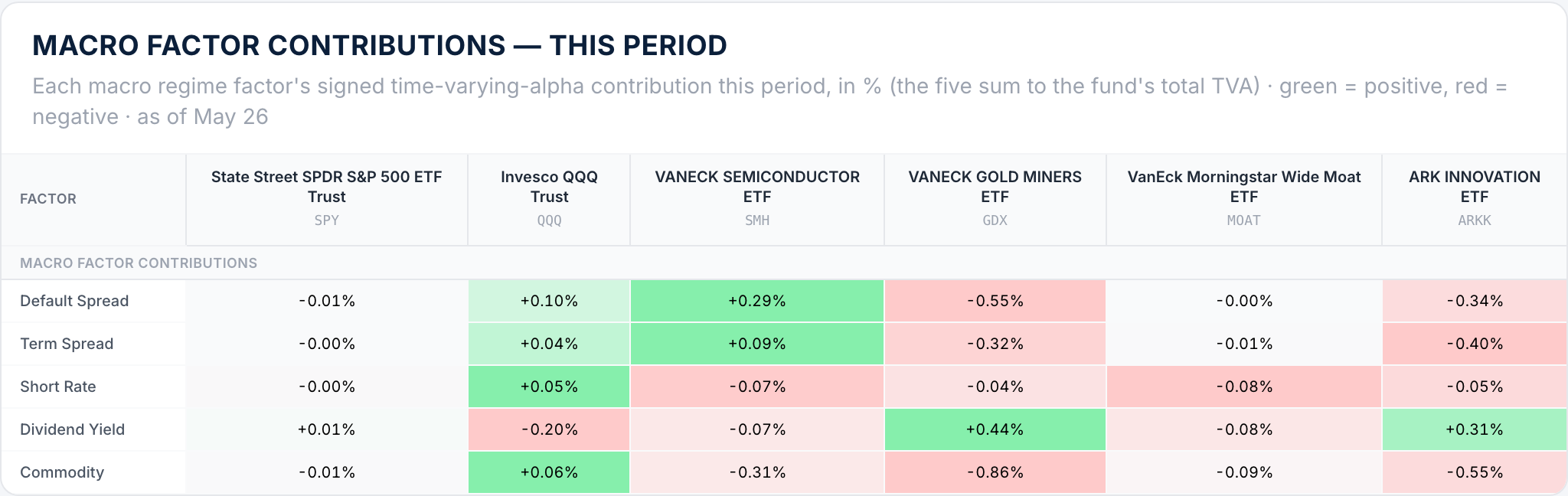

The macro engine

Alpha depends on the regime

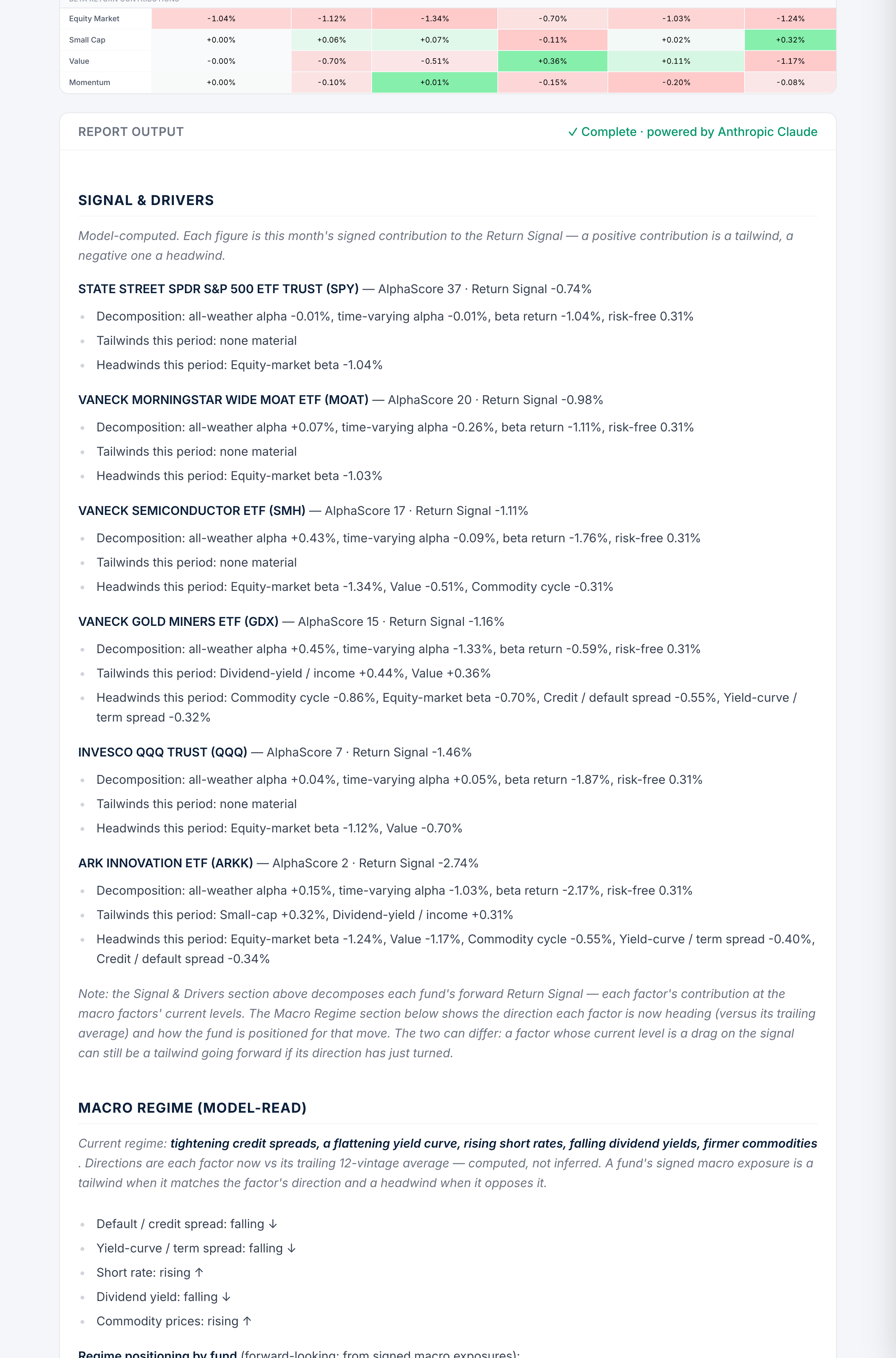

Most models estimate one static alpha per fund. AlphaPredictor® splits it in two: all-weather alpha, earned in any environment, and time-varying alpha — the part a fund earns in this macro environment, driven by its sensitivity to five regime factors: default spread, term spread, short rate, dividend yield and commodities.

Below, each fund's monthly Return Signal is split into the contribution from every regime factor — green where a factor added to the signal this month, red where it subtracted. The model re-estimates these as the regime shifts.

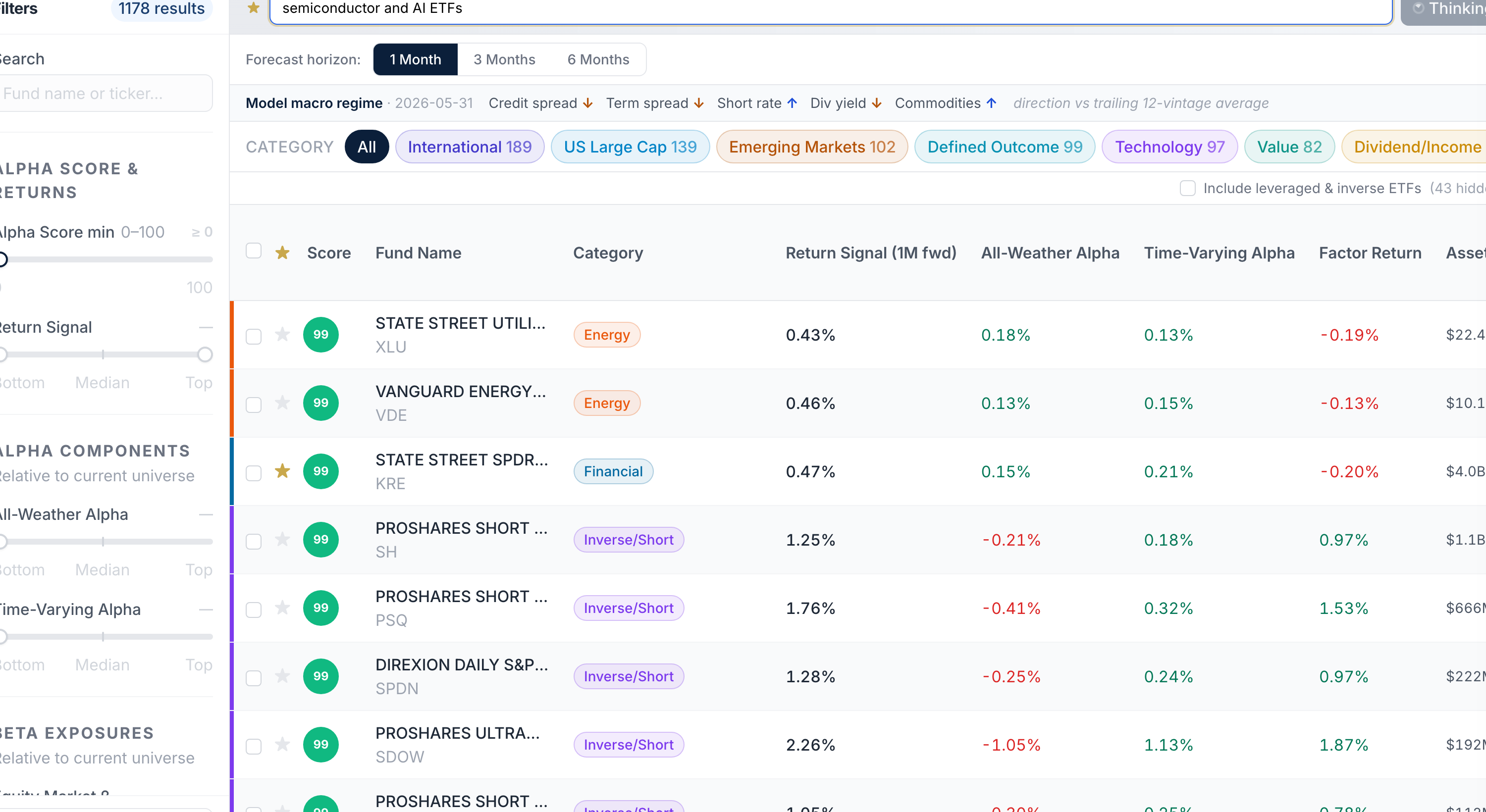

The AlphaScore™

A single, defensible number for every fund

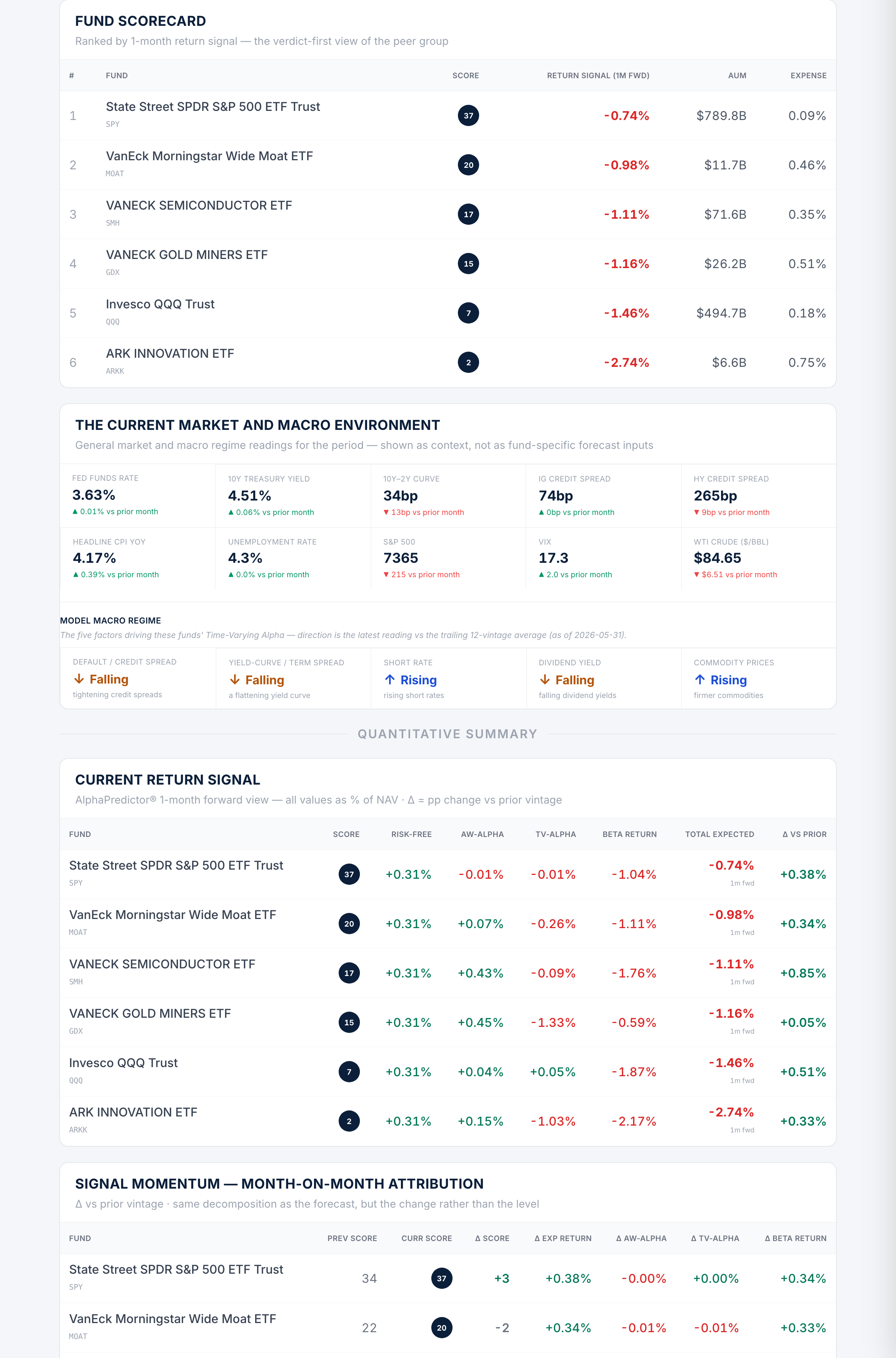

Every ETF's return signal for the coming month is ranked into a percentile against the full universe — 100 = the strongest signal, 0 = the weakest — and broken into the components that drive it: all-weather alpha, time-varying alpha, and factor return. Sort 1,221 funds in one view, or filter to a category and find the strongest names instantly.

- ▸ Return signal decomposed into alpha vs beta, not a black box

- ▸ Factor and macro exposures as z-scores against the whole universe

- ▸ Natural-language screening — "cheapest tech with strong momentum"

Drill into any fund

Every number traceable to the model

Click a fund and the full picture opens: the return signal broken into all-weather alpha, time-varying alpha, factor return and the risk-free rate — then the factor and macro exposures behind it, each scored against the whole universe. Here, energy's XLE earns a 98 AlphaScore from a positive alpha and value tilt, even as its equity-market beta is a drag this month.

- ▸ Expected-return waterfall: where every basis point comes from

- ▸ Beta and macro sensitivities as ±σ z-scores vs all 1,221 funds

- ▸ Trailing performance, AUM, expense ratio and benchmark in one place

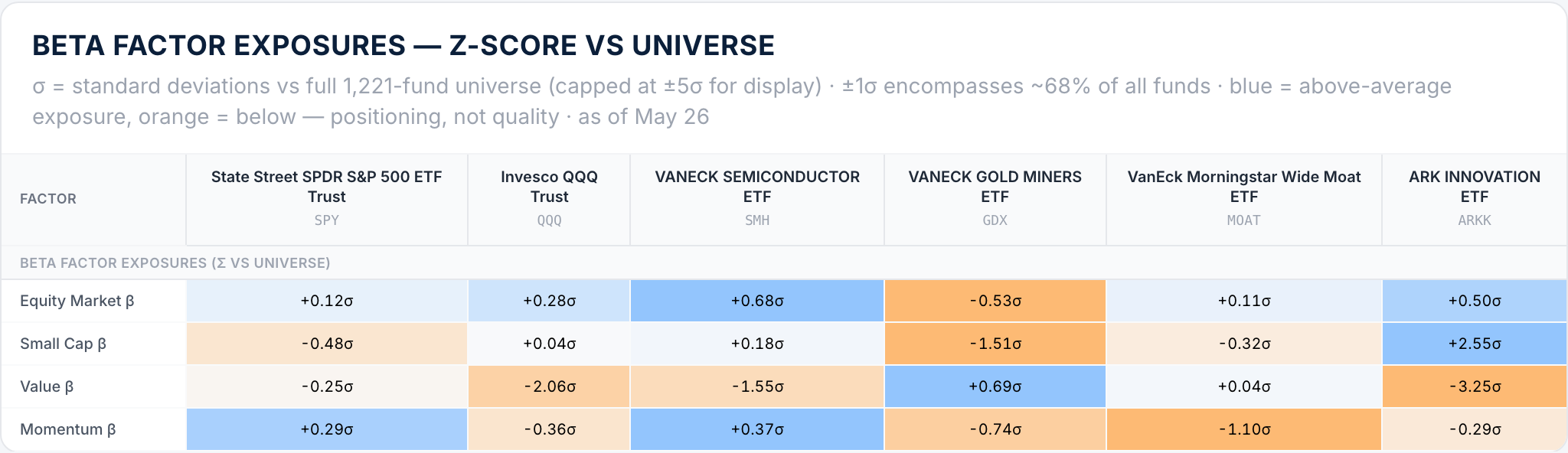

Factor heat maps

Every exposure, mapped against the universe

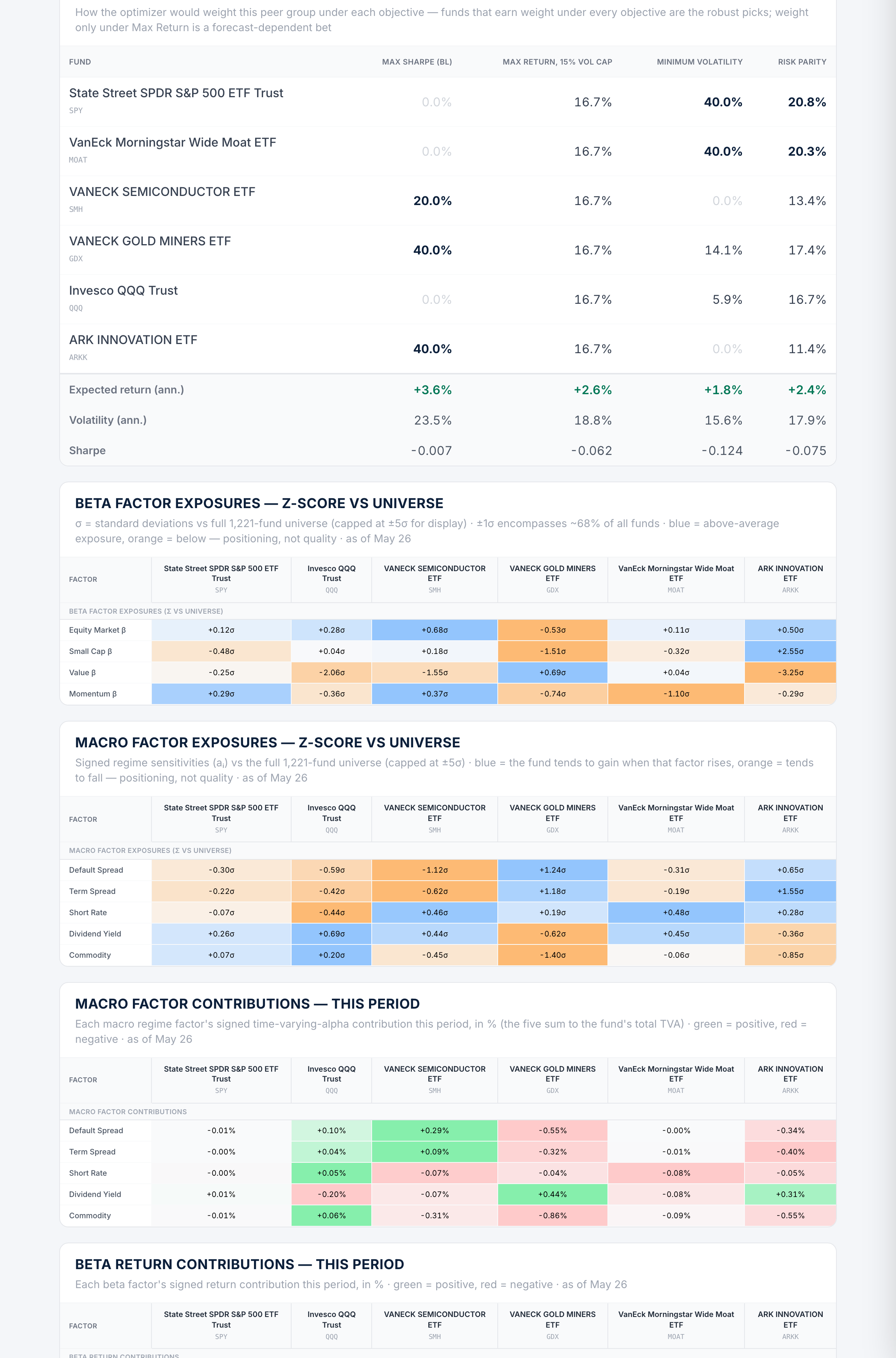

See each fund's tilt to the equity-market, size, value and momentum factors as z-scores against all 1,221 funds. Blue runs above average, orange below, so a peer group's positioning reads in a single glance.

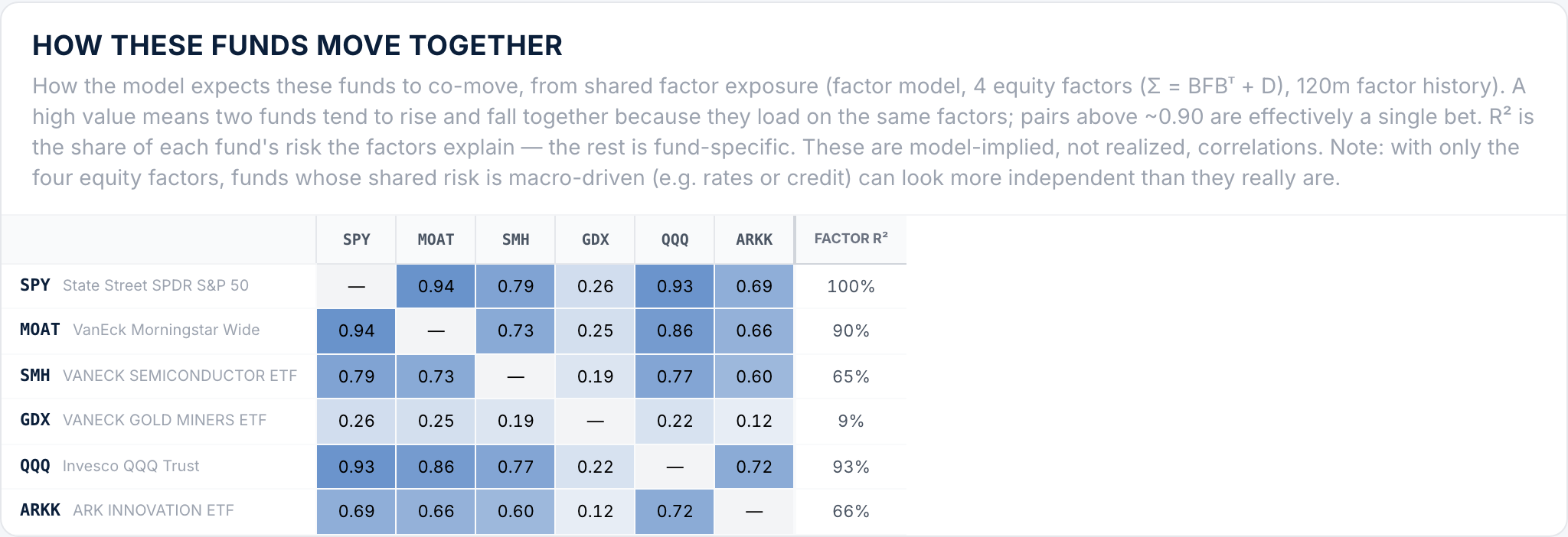

See the overlap

Know which bets are really the same bet

A factor-structured covariance shows how any set of funds actually move together — and how much of each fund's risk is explained by the four equity factors. Below, VGT and QQQ correlate 0.90 — near-duplicates — while energy and utilities diversify the book. It's the diversification check most screeners can't do.

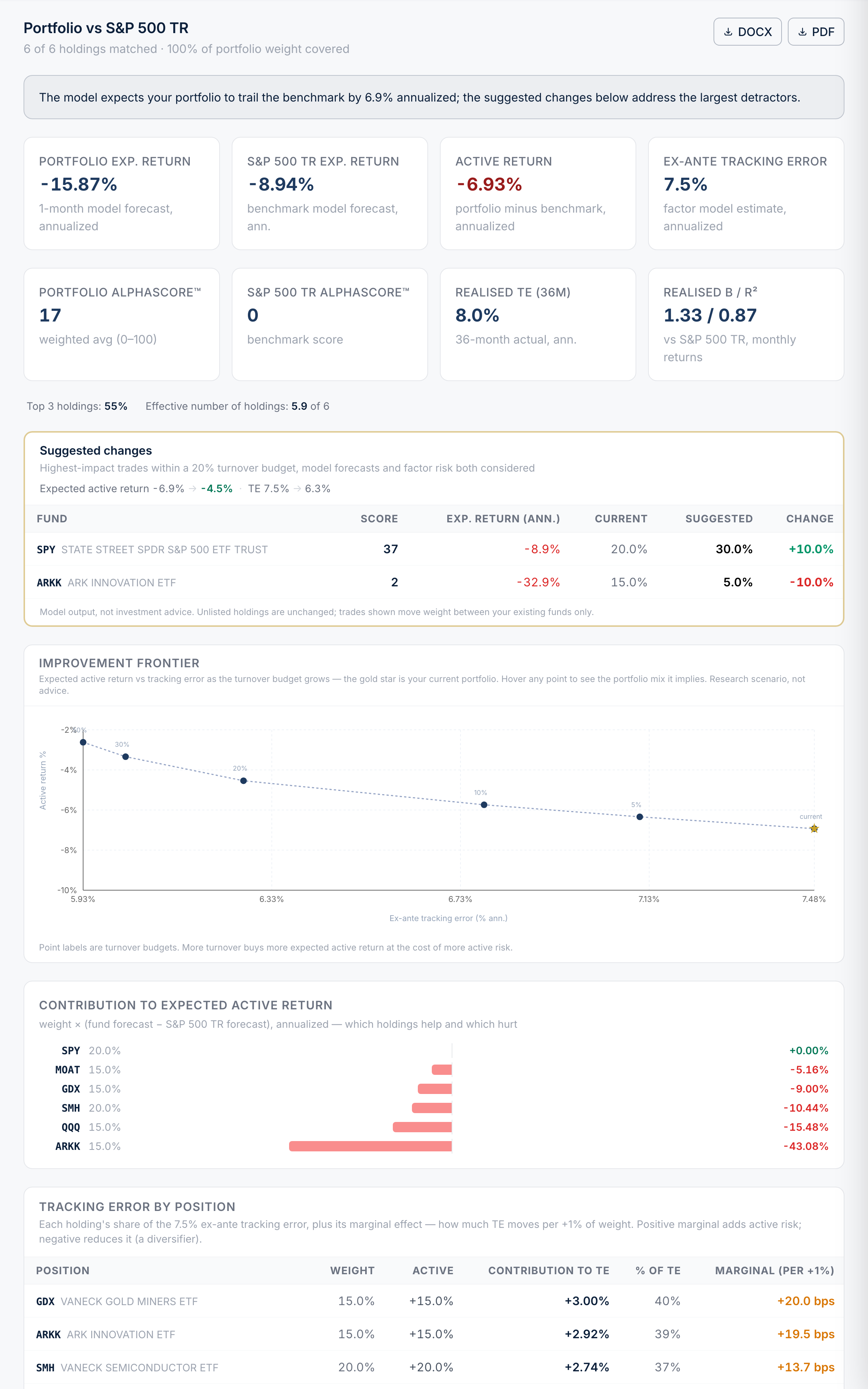

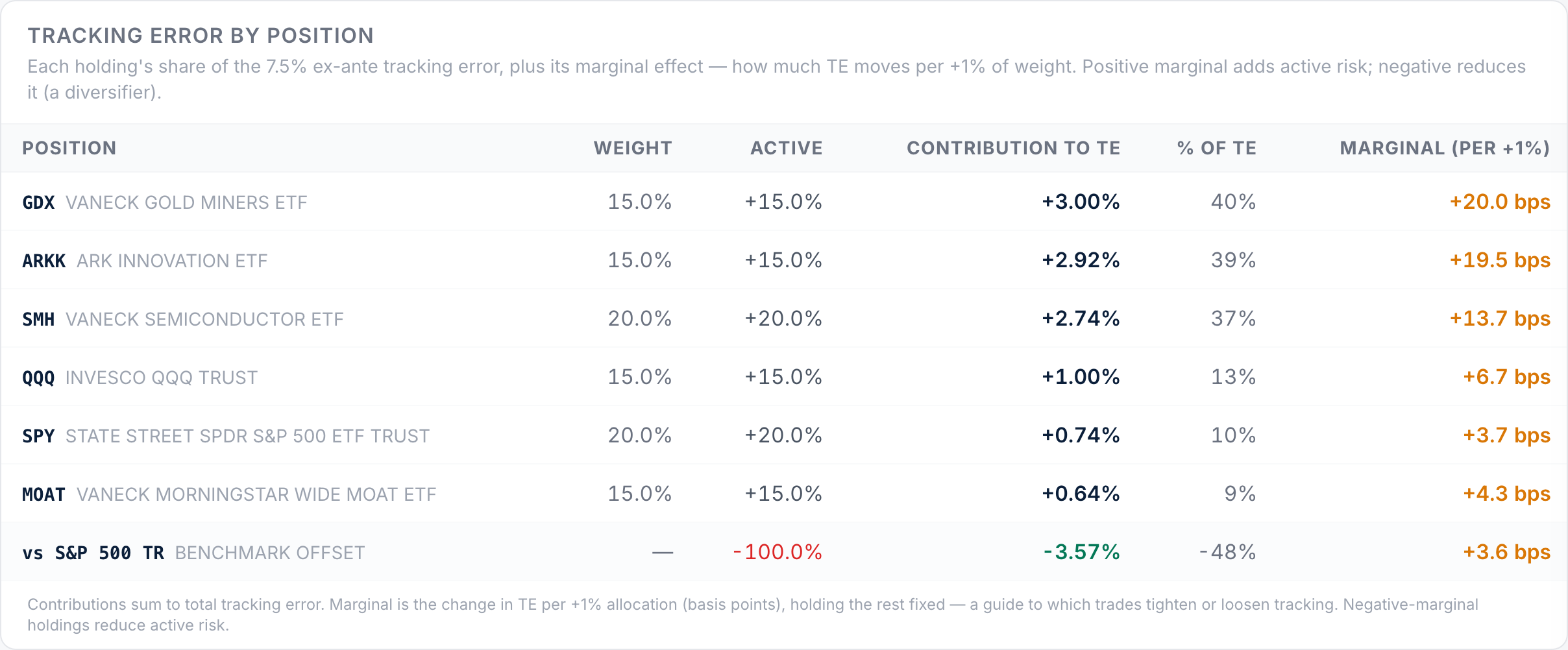

Portfolio analyzer

Build it, stress-test it, see what to change

Paste any portfolio and measure it against a benchmark: expected active return, tracking error, and a per-holding breakdown of which positions drive your active risk — and which way each trade moves it. The optimizer proposes the highest-impact changes within a turnover budget.

- ▸ Contribution & marginal contribution to TE, by position

- ▸ Five objectives, including max information ratio vs a benchmark within a tracking-error budget

- ▸ Suggested trades to tighten or loosen tracking

Portfolio construction

One peer group, four ways to weight it

The optimizer proposes allocations under four objectives at once — max Sharpe, max return within a volatility cap, minimum volatility, and risk parity — over a factor-aware covariance. Funds that earn weight under every objective are the more robust candidates; weight only under max-return signals a forecast-dependent position.